- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Key Points

What it is

A structured early‑retirement income approach that uses distributing ladder ETFs to create predictable cash flow and bridge the years before Social Security.

Why it matters

Reliable cash flow reduces anxiety and behavioral pressure, helping clients avoid early Social Security claims and irreversible trade‑offs that can diminish lifetime income.

Where it's going

Advisors are increasingly adopting purpose‑built, transparent income structures that align portfolio cash flows with real‑world spending needs to drive better long‑term outcomes.

For many clients, retirement doesn’t unfold neatly on a spreadsheet. The shift from earning a paycheck to relying on portfolio income often brings heightened market sensitivity and real anxiety around “getting it right.”

One of the most consequential decisions clients face during this transition is when to claim Social Security. While delaying benefits can meaningfully increase lifetime income, short-term cash‑flow pressure often pushes clients to claim earlier than planned.

Advisors increasingly recognize that the challenge isn’t understanding math. It’s managing behavior during the most fragile years of retirement.

Question: Why are the first few years of retirement such a critical planning period for advisors and clients?

Answer: The early years of retirement represent a permanent inflection point. Decisions made during this window, particularly around income sourcing and Social Security timing, can’t easily be undone. Clients are shifting from accumulation to decumulation and often facing higher discretionary spending, just as their paychecks stop. Without a structured income plan, short-term cash‑flow pressure can force long-term trade‑offs that materially reduce lifetime income.

Q: Why do so many retirees claim Social Security early, even when waiting could improve lifetime benefits?

A: Clients who claim early often feel uncertain about cash flow, market volatility, or the durability of their portfolio. Early retirement spending, fear of outliving assets, and lack of predictable income sources create anxiety. Claiming Social Security early feels like a guaranteed solution, even though it permanently reduces benefits. Advisors frequently recognize the trade‑off, but without a clear income bridge, clients struggle to wait.

Q: How can distributing ladder ETFs help advisors address this challenge?

A: Distributing ladder ETFs are designed to create time‑bound, predictable cash flow that can bridge income gaps in early retirement. By returning principal annually as bonds mature, alongside monthly income, these strategies allow advisors to replace income temporarily without forcing clients to lock in lower Social Security benefits. The structure helps align portfolio cash flows with known spending needs, reducing the pressure to draw from Social Security or sell risk assets at inopportune times.

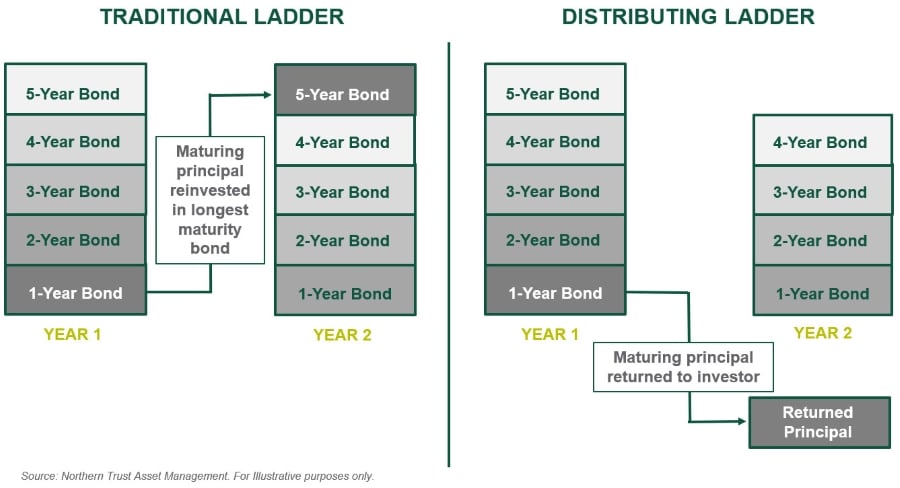

Q: How do distributing ladder ETFs differ from traditional bond ladders?

A: Traditional bond ladders are effective but operationally complex, especially at scale. Distributing ladder ETFs deliver similar duration and interest rate management benefits, but with added clarity and simplicity. Instead of reinvesting maturities, principal is systematically returned to investors on a predictable annual schedule. This makes the cash flow profile easier to communicate and easier for clients to understand. For advisors, it reduces implementation friction while preserving the core laddering benefits.

Q: What benefits do advisors see from using distributing ladder ETFs?

A: From an advisor’s perspective, these strategies simplify portfolio construction into a single, transparent allocation, scale efficiently across multiple client accounts, reduce reliance on tactical market timing, and support more consistent planning conversations year over year. The ETFs are diversified and actively managed within a defined maturity framework. Advisors gain operational efficiency without sacrificing credit quality or cash‑flow discipline.

Funding early retirement to delay claiming

Bridging the Social Security gap with a five-year Distributing Ladder to avoid penalties can provide investors enhanced Social Security cash flow from age 67 onward.

Source: Northern Trust Asset Management. There will be no further distributions from the ladder ETF after 5 years.

Q: How do these strategies benefit clients directly?

A: For clients, the benefits are tangible and behavioral. Predictable annual return of principal supports known spending needs and monthly income continues throughout the ladder’s life. Anxiety around market volatility and sequencing risk is reduced, and clients gain greater confidence to delay Social Security and optimize lifetime income. Perhaps most importantly, clients gain visibility into how much income and principal they’ll receive and when, which can help them stay committed to a long-term plan.

Q: Can you give an example of how this works in practice?

A: Consider an early retiree who leaves the workforce at 62 but has the option to delay Social Security until full retirement age. By allocating a portion of assets to a five-year distributing ladder ETF, the advisor can replace income during those years. When Social Security begins later, the client locks in a meaningfully higher monthly benefit for life. Over time, the increase in guaranteed income can offset the assets used to bridge the gap, improving long-term financial security without increasing portfolio risk.

Q: Are these strategies only useful for Social Security planning?

A: Not at all. While Social Security bridging is a common use case, advisors also use distributing ladder ETFs to fund required minimum distributions, immunize specific spending goals, support education or multiyear gifting strategies. Any scenario involving recurring, time defined cashflow needs can benefit from this structure.

Q: What should advisors keep top of mind when considering these strategies?

A: Early retirement decisions have an outsized impact. Distributing ladder ETFs aren’t about chasing yield; they are about aligning assets with purpose. When advisors can clearly define which years of spending are already funded, they give clients confidence. That confidence creates space for better decisions, better outcomes, and more durable client relationships.

Northern Trust Tax-Exempt Distributing Ladder ETFs | Northern Trust Inflation-Linked Distributing Ladder ETFs |

|---|---|

MUNA 5 years (2030)

|

TIPA 5 years (2030)

|

Fees: 18 BPS** | Fees: 10 BPS** |

*Individual bonds carry an obligation to fully return principal to investors at maturity, however ETFs have no such obligation. The net asset value of the ETFs will decline over time as income payments are made to shareholders.

**18 basis points (BPS, or 0.18%) and 10 basis points (BPS, 0.10%) refers to both net and gross expense ratios. Interest on municipals is exempt from federal income tax but may be subject to state and local tax. This information is general in nature and should not be construed as tax advice.

Related Content

Contact Us

Interested in learning more about our expertise and how we can help?

IMPORTANT INFORMATION

Before investing, carefully consider the investment objectives, risks, charges, and expenses. This and other information is in the prospectus and a summary prospectus, copies of which may be obtained by visiting www.flexshares.com or calling 855-353-9383. Read the prospectus carefully before you invest. Northern Funds Distributors, LLC, distributor. Northern Funds Distributors, LLC and FlexShares are not affiliated with Northern Trust.

All investments are subject to investment risk, including the possible loss of principal amount invested. Investments do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Individual bonds carry an obligation to fully return principal to investors at maturity, however ETFs have no such obligation. The net asset value of the ETFs will decline over time as income payments are made to shareholders.

Not FDIC insured | May lose value | No bank guarantee

As with any fund, it is possible to lose money on an investment in the Fund. An investment in the Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation, any other government agency, or The Northern Trust Company, its affiliates, subsidiaries or any other bank.

ETFs are subject to additional risks that do not apply to conventional mutual funds, including the risks that the market price of an ETF’s shares may trade at a premium or discount to its net asset value, an active secondary trading market may not develop or be maintained, or trading may be halted by the exchange in which they trade, which may impact an ETF’s ability to sell its shares. Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns.

RISKS APPLICABLE TO BOTH TAX-EXEMPT AND INFLATION-LINKED DISTRIBUTING LADDER ETFs

{{credit_risk}}

Fluctuation of Yield and Principal Payment Risk is the risk that the Fund, unlike a direct investment in a bond that has a level coupon payment and a fixed payment at maturity, will make distributions of income that vary over time. Unlike a direct investment in bonds, the breakdown of returns between Fund distributions are not predictable at the time of your investment.

Fund Termination Risk is the risk that, unlike an investment in a traditional investment company with perpetual existence, the Fund is designed to liquidate in the terminal year and thus a shareholder of the Fund will not receive distributions from the Fund beyond the terminal year.

{{liquidity_risk}}

{{non_diversification_risk}}

Return of Capital/Distribution Risk is the risk that the Fund’s distributions will involve a return of capital, which, although not currently taxable, may lower a shareholder’s basis in the Fund’s shares, thus potentially subjecting the shareholder to future tax consequences in connection with the sale of Fund shares, even if sold at a loss to the shareholder’s original investment.

Small Fund Risk is the risk that the Fund will not grow to or maintain an economically viable size, in which case it may liquidate prior to the anticipated liquidation date in the terminal year, thus impacting the Fund’s ability to achieve its investment objective.

RISKS APPLICABLE TO NORTHERN TRUST TAX-EXEMPT DISTRIBUTING LADDER ETFS

Municipal Investments Risk is the risk that the value of a municipal security generally depends on the financial and credit status of the issuer. Constitutional amendments, legislative enactments, executive orders, administrative regulations, voter initiatives, and the issuer’s regional economic conditions may affect a municipal security’s value, interest payments, repayment of principal and the Fund’s ability to sell the security.

Municipal Market Volatility Risk is the risk that the Fund may be adversely affected by volatility in the municipal market. The municipal market can be significantly affected by adverse tax, legislative, political or public health changes and the financial condition of the issuers of municipal securities.

Municipal Tax Liability Risk is the risk that shareholders of the Fund could be subject to tax liabilities. The Fund will invest in municipal securities in reliance at the time of purchase on an opinion of bond counsel to the issuer that the interest paid on those securities will be excludable from gross income for regular federal income tax purposes.

RISKS APPLICABLE TO NORTHERN TRUST INFLATION-LINKED DISTRIBUTING LADDER ETFS

Inflation-Indexed Securities Risk is the risk that the value of inflation protected securities, such as TIPS, generally will fluctuate in response to changes in real interest rates, generally decreasing when real interest rates rise and increasing when real interest rates fall. In addition, interest payments on inflation-protected securities will generally vary up or down along with the rate of inflation.